Startup Valuation: How to Turn Numbers on Paper into Real Investments

Why is Startup Valuation the Key to Success?

What do the collapse of Theranos and the rise of Airbnb have in common? Both scenarios hinge on one critical factor—startup valuation. The former failed due to inflated projections, while the latter soared thanks to precise calculations. But do you know what’s even more alarming? One in four startups shuts down precisely because of valuation errors. Imagine: you ask for 5 million for 10% of the company (valuation of 50 million), but venture capital firms are only willing to invest 2 million for 10% (valuation of 20 million). A gap of 30 million threatens to fail the deal. Revising the business valuation methods (for example, through comparison with similar companies or discounted cash flow analysis) helped justify the valuation of 40 million — and the deal was done. This is where valuation experts come in, using data-driven insights to ensure a more accurate and defendable valuation.

Why do even brilliant ideas fail because of numbers on paper? The answer is simple: startup valuation isn’t just math; it’s a balance between data and belief in potential. Suppose you’ve just launched an MVP and are already dreaming of a billion-dollar valuation. Business valuation services, however, can help provide a more grounded perspective. VC firms, however, see things differently: they care less about your ambitions and more about market multiples, discounted cash flows, and risks. How do you convince them your startup is worth the millions you claim? And more importantly, how do you avoid fatal mistakes?

A detailed business plan often includes not just your business model, but also a strategic view of your growth potential. Business plan writers can assist in refining your pitch, ensuring your startup’s valuation aligns with industry standards and investor expectations. Without the right support and expert advice, it’s easy to inflate your value or downplay your weaknesses. A balanced valuation is key to securing funding and maintaining investor confidence.

Ultimately, securing funding and scaling your business requires more than just a good idea—it requires strategic startup valuation services that align your vision with realistic growth metrics. By using expert services, you can avoid common valuation errors that could cost you dearly and ensure you’re presenting your company at the right value for investors and your future.

Let’s explore why startup valuation is a minefield for founders, the three methods venture capital firms use, and how to turn dry numbers into real investments. Ready to dive in?

Startup and Its Valuation: Basic Concepts

What is a Startup?

Imagine you’ve created an app that replaces all loyalty cards in the world with a single digital platform. You don’t have revenue yet, but you already have 100,000 users. That’s a startup—like Uber in 2010: a revolutionary idea that disrupts the market but lacks a proven business model.

If your product doesn’t make competitors nervous or have customers saying, “How did I ever live without this?”—it’s not a startup. It’s just a business. A startup is always about risk, scale, and speed. For example, a California-based startup developed an AI system for diagnosing cancer from scans. Revenue? Zero. But the business valuation is $20 million. Why? Because the healthcare market is $10 trillion, and its technology saves doctors 70% of their time. This is where startup valuation experts come in, using their expertise to determine the value of the company based on its potential, not just its current revenue.

Why is startup valuation more difficult than business valuation?

Valuing McDonald’s is easy: there’s profit, franchises, and a history. But how do you determine the value of a startup that won’t earn its first dollar until a year from now? Suppose you have a SaaS platform with 5,000 free users. An investor asks, “Why should I believe they’ll start paying?”

Answering is tough, and here’s why:

- No data. You can’t show past financial reports.

- Forecasts lie. Research shows that 9 out of 10 startups get revenue projections wrong in the early stages.

- Subjectivity. One venture fund will value you at $5 million, another at $2 million, and both could be right.

For example, an EdTech startup from Texas projected $1 million in revenue by year three, but actual numbers were four times lower. Why? They didn’t account for seasonal demand for online courses.

Why Do Investors Care About Startup Valuation?

Why are venture funds willing to invest $10 million in a company that hasn’t earned a cent yet? The answer is simple: they’re not buying current metrics but the potential for 10x growth.

Imagine you’re asking for $2 million for 10% ($20 million valuation). The investor agrees but only if you can prove the company will be worth $200 million in five years. How? Through discounted cash flows, market multiples, or the potential to capture 5% of the TAM (Total Addressable Market).

For example, a biotech startup from Boston raised $15 million at the Idea stage. Angel investors believed not in revenue (there was none), but in patents and a team of ex-Pfizer employees. Three years later, they were bought for $450 million. Business valuation services helped VC firms look closely at the potential for growth, rather than just current financials.

Startup Valuation Approach Methods: Tools and Methods

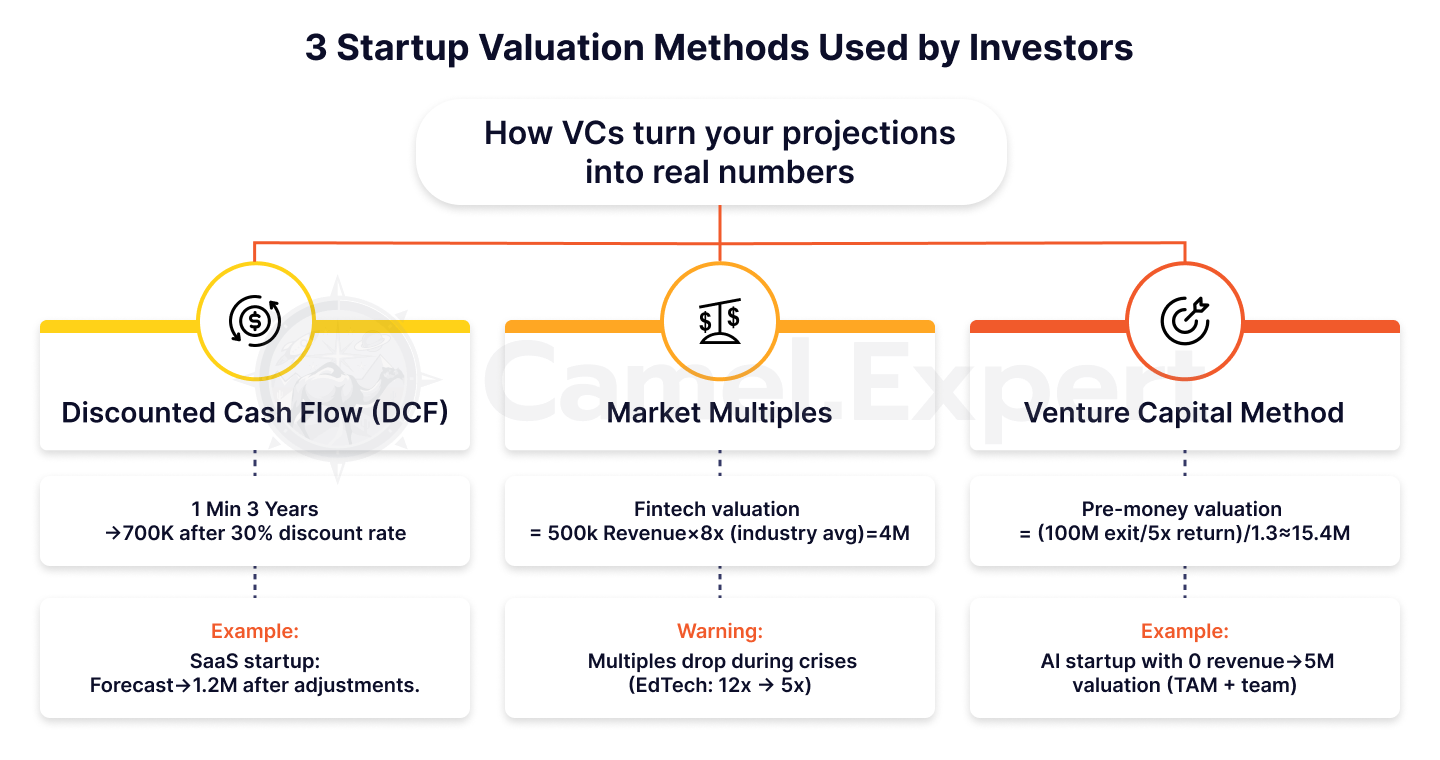

3 Startup Valuation Methods Used by Venture Capital Firms

1. Discounted Cash Flow (DCF)

Why don’t investors trust your revenue forecasts? Because startups are risky, and risk costs money. Suppose your SaaS project promises $1 million in revenue in 3 years. But the investor discounts these figures by 30% per year, and in their calculations, $1 million turns into only $700 000.

Example: A California-based startup developed a platform for remote teams. It projected $2 million revenue by year 3, but after discounting (25% per year) the amount was reduced to $1.2 million.. The deal was saved only by proof of 15% monthly MRR (Monthly Recurring Revenue) growth.

2. Market Multiplier

Imagine your Miami-based fintech startup is similar to Revolut in 2016. How do you value it? Angel investors compare you to similar companies and apply a multiple like EV/Revenue. If the industry average is 8x and your revenue is $500k, the valuation would be $4M.

But be cautious: multiples change. In 2021, the EdTech sector traded at 12x, but after the 2022 crisis, it dropped to 5x. How do you avoid miscalculations? Always look at recent deals in your niche.

3. Venture Capital Method (VC Method)

How do you turn an investor’s desired return into a valuation? Suppose a fund wants a 5x return in five years. If the exit target is a $100 million sale, then:

Pre-money valuation = ($100 millions/ 5) / (1 + 0.3) = $20 mln/ 1.3 ≈ $15.4 mln.

Sounds complicated? It is. But this is how VCs value pre-seed startups. For example, a New York-based AI startup received a valuation of $5 million, although there was no revenue. Investors believed in TAM ($50 billion) and a team of ex-Google employees. This is where seed funding companies play a crucial role, providing the initial capital to support the potential growth and success of such startups.

Table 1: Comparison of Startup Valuation Methods

| Method | Description | Pros | Cons | Example |

| DCF | Forecasting cash flows with risk adjustments (discounting). | Consider long-term potential. | Requires accurate forecasts. | SaaS startup: 1M→700K. |

| Market Multiples | Comparing with similar companies (EV/Revenue, EV/EBITDA). | Quick to apply. | Depends on market fluctuations. | Fintech: 500K×8x=4M. |

| VC Method | Startup valuation based on investor’s target return. | Easy for investors to understand. | Ignores current metrics. | Pre-money valuation: 5M→100M. |

How to Use Hybrid Approaches?

“What if we combine several methods?” you might ask. That’s the right question! A hybrid approach is your insurance against mistakes.

Step 1: Calculate the startup’s value using DCF with conservative forecasts.

Step 2: Cross-check the result using market multiples. If the gap exceeds 30%, investigate the reasons.

Step 3: Add qualitative factors. Do you have patents? Multiply the valuation by 1.2. Don’t have any? Subtract 15%.

Example: A Boston-based healthcare startup used a DCF ($12 million post-money valuation) and multiples ($15 million). But investors gave $18 million — thanks to an exclusive partnership with the Mayo Clinic.

Valuing a Startup with No Revenue: How to Do It?

Why is it a Challenge?

How do you convince an investor that your AI-powered app is worth $10 million when you haven’t sold a single subscription? It sounds like a gamble, but this is exactly how Uber, Airbnb, and even DeepMind started. The problem is that a startup without revenue is pure potential: no metrics, no history, just belief in the idea. This is where VC firms come in—they specialize in recognizing and backing that potential, even when the numbers don’t yet support it.

Suppose you’ve just launched an MVP and are asking for $5 million. The investor asks: “Why should I believe your AI cancer diagnostics tool will be in demand?”

It’s hard to answer, but not impossible. For example, a Boston-based startup justified a $12 million valuation without revenue by presenting patents and pilot agreements with two major clinics.

4 Key Factors

1. Product: It’s Not About Features, It’s About Uniqueness

Forget listing features. Showcase your technological edge. For instance, DeepMind raised $600 million before monetization thanks to algorithms that beat humans at Go. Investors pay for technologies no one else has.

2. Team: “We Bet on Founders, Not Ideas”

This is a quote from a Sequoia Capital partner. If your team includes a former Google employee or a Stanford graduate, your valuation could increase by 30-50%.

3. Market Size: Your Trump Card

In 2011, Uber was valued at $60 million without revenue. How? They proved that the TAM of the taxi market is $4.7 trillion. Even 1% of this market is $47 billion.

4. Competitors: The Fewer, the Better

Imagine you’ve created the only platform for training AI models on quantum computers. No competitors? Your startup valuation could skyrocket by 70%.

Table 2: Factors for Valuing a Startup with No Revenue

| Factor | What’s Evaluated | Example |

| Product | Technological advantage, patents. | DeepMind: Algorithms for playing Go. |

| Team | Founders’ experience, expertise. | Ex-Google/Stanford experts → +30-50% valuation. |

| Market Size | TAM, SAM, SOM. | Uber: TAM 4.7T→60M valuation. |

| Competitors | Product uniqueness. | AI platform for quantum computing. |

The Uber Case

In 2011, Uber was just an app for booking black cars in San Francisco. Revenue? Zero. But investors valued the startup at $60 million. Why?

- TAM: The taxi and ridesharing market was $4.7 trillion.

- Expansion Speed: A plan to enter 10 cities in 2 years.

- Team: Travis Kalanick had already sold a startup for $23 million.

Today, Uber is worth $90 billion. Was It worth risking $60 million in 2011? The answer is obvious.

Startup Revenue: Myths and Reality

Frequently Asked Questions

“Why is my startup with $200k in revenue valued lower than a competitor with no revenue?” is one of the most common questions.

The answer is simple: Revenue isn’t value. If you spend $2 to acquire a customer who brings in $1, you’re bankrupt.

Suppose you’ve launched an MVP marketplace. In the first month, you generate $50k in revenue. But your CAC (Customer Acquisition Cost) is $100, and your LTV (Lifetime Value) is $80.

What will investors calculate? You’re losing $20 per user. Result? Your “successful” revenue model becomes a red flag.

Case Study: A Silicon Valley startup generated $1 million annually, but its CAC was three times higher than its LTV. After correcting the monetization model, its startup valuation increased by 40%.

When Revenue Hurts?

Imagine your e-commerce startup shows $500k in revenue, but your CAC is 150, and your LTV is $80. Investors will run. Why? Because revenue without profitability is a pyramid scheme.

In 2022, a Los Angeles startup raised $2 million based on $700k in revenue. A year later, investors demanded their money back—every dollar of revenue “cost” them $1.50 in losses.

How to avoid this? Focus not on revenue but on Unit Economics.

Tip: If your margin is below 20%, focus on increasing it rather than increasing revenue.

How Does the Revenue Multiplier Change Perceptions of Value?

Why are SaaS startups valued at 8-12x EV/Revenue, while retail is valued at just 1-2x? It all comes down to potential. SaaS scales almost cost-free, while retail depends on logistics and warehouses.

Example:

- A New York startup with $2 million in revenue was valued at $24 million (12x). Its “secret sauce” was 95% margins due to automation.

- A Miami florist with $1 million in revenue is valued at only $1.5 million (1.5x).

Want a high multiplier? Create a product that scales like WhatsApp.

Table 3: Revenue Multipliers by Industry

| Industry | EV/Revenue | Reason |

| SaaS | 8-12x | High margins, scalability. |

| E-commerce | 1-2x | Dependence on logistics and costs. |

| FinTech | 5-8x | Rapid growth, regulatory risks. |

| Biotech | 3-6x | Long product development timelines. |

Presenting Startup Valuation Results to Investors

5 Mistakes That Kill Your Pitch

- Unrealistic Forecasts: “Revenue will grow 300% in a year.”

Suppose you’ve just launched an MVP and promise explosive growth. But investors know: such numbers are only possible with a viral coefficient >2 (where each user brings in two new ones). Without data, it’s just fantasy. Example: A California startup claimed 500% revenue growth but couldn’t explain how to achieve it without increasing CAC. Result? Investors doubted their calculations. - Ignoring Risks: “Our product is perfect; competitors are hopeless.”

Imagine an investor asks, “What if regulators ban your technology?” If you’re unprepared to answer, your startup valuation loses credibility.

Case Study: A Miami-based crypto startup didn’t account for regulatory risks. When the SEC introduced new rules, the deal fell apart. - Lack of Benchmarks: “We’re like SpaceX, but better.”

If you’re asking for a SpaceX-like valuation, be ready to show comparable technological risks and a patent portfolio. Comparisons without proof are a red flag. - Weak Method Justification: “We used DCF because everyone does.”

Why did you choose multiples over discounted cash flow? Explain how the method aligns with your business model. - Unpreparedness for Questions: “I didn’t expect that…”

Investors will scrutinize every number. If you don’t know how you calculated TAM or CAC, the deal is over.

Table 4: Startup Valuation Presentation Mistakes and Solutions

| Mistake | Consequences | How to Fix It? |

| Unrealistic Growth Forecasts | Loss of investor trust. | Use retention and virality data. |

| Ignoring Risks | Deal falls apart at the first crisis. | Add scenario analysis (“What if?”). |

| Lack of Benchmarks | Investors won’t understand your uniqueness. | Compare with 3-5 analogs in your niche. |

Turning Numbers into a Story: How to Make Investors Believe

“We’re not renting out homes—we’re creating a new way to travel,” declared Airbnb’s founders in 2008. Their valuation was $2.4 million, but the story of a “world without middlemen” won over investors.

How to replicate this success?

- Tie Numbers to a Mission: For example: “Our startup will reduce CO₂ emissions by 1 million tons by 2025—equivalent to taking 200,000 cars off the road.”

- Use Analogies: Suppose you’re building a SaaS for small businesses. Say, “We’re like Shopify, but for online education.”

Case Study: A Boston biotech startup raised $10 million by comparing its technology to “GPS for DNA.” Investors remembered the metaphor, not the dry calculations.

Table 5: Examples of Startup Valuation for Famous Startups

| Startup | Year | Stage | Valuation | Key Factor |

| Uber | 2011 | Early-stage | $60 million | TAM $4.7T, expansion speed. |

| Airbnb | 2008 | Seed | $2.4 million | Network effects, mission. |

| Slack | 2014 | Series A | $1.1 billion | DAU (Daily Active Users) growth. |

| SpaceX | 2008 | Early-stage | $1 billion | Technological risks and patents. |

Venture Capital and Valuation: What Are Investors Hiding?

Valuation Flexibility: Why Does the Startup Stage Matter?

Why are investors willing to pay millions for a slide deck with an idea at the seed stage but demand detailed metrics at Series A? It’s simple: valuation is a game with ever-changing rules. At the seed stage, seed funding companies are often betting on the potential of the idea and the team behind it, rather than on hard data and performance metrics.

- Seed Stage: The team is everything. Suppose you only have an MVP, but your team includes a former Apple engineer and a Y Combinator alum. That alone could add $1–2 million to your valuation.

Example: a startup from San Francisco raised $2 million without a product, because the founders had previously sold a project for $10 million. - Series A: Unit economics rule here. If your CAC (Customer Acquisition Cost) is = $50, an LTV = $200, your valuation will soar. If not, even a brilliant idea won’t save you.

Rhetorical Question: Want a high valuation at an early stage? Build a team that makes investors believe in the impossible.

Adjustments in Practice: Why $50 Million Turns into $30 Million?

“We’re ready to invest, but the total valuation will be $30 million, not $50 million”—a phrase half of all founders have heard. Why? Investors factor in liquidity and risks.

Example: A Los Angeles startup developed a VR training platform. Pre-money valuation— $50 million. But the fund cut it to $35 million, arguing: “ The VR market VR is unstable, and there have been few exits so far.”

How to Protect Yourself? Study the average multiples in your niche and build in a 20% buffer.

Tip: If an investor demands a discount, ask, “How would the valuation change if we signed a contract with a Fortune 500 company?”

3 Scenarios Where Valuation Kills the Deal

- “We Want to Be Like SpaceX!”

Asked for $100 million like Elon Musk? Be ready to show technological risks and a patent portfolio. Otherwise, investors will doubt your credibility. - Macroeconomic Collapse.

In 2022, the Fed raised interest rates, and startup valuations dropped by 30-40%. Even the best product can’t save you if the market is in panic mode. - Unproven Metrics.

“We’ll capture 10% of the market in a year” sounds great. But without retention or virality data, it’s just empty words.

Example: A Texas startup lost a $20 million deal due to an inflated TAM. Investors checked the calculations and found the actual market was five times smaller.

Startup Valuation Method as Art and Science

Startup valuation isn’t just numbers in a spreadsheet. It’s a balance between cold calculations and belief in the future. Can you trust such a delicate task to Excel formulas?

Ask the Silicon Valley founder who lost $3 million due to TAM calculation error. Or a startup from California, who raised $5 million after an audit from Camel Expert.

Want to know your startup’s real value? Camel Expert will conduct an audit, prepare you for negotiations, and show you how to avoid 90% of mistakes.

P.S. Remember: Airbnb was once valued at $2.4 million. Today, it’s worth $90 billion.

The question isn’t how much your startup is worth now—it’s what story you’ll tell investors.

Conclusion

Valuing a startup company, especially a pre-revenue startup, is a complex yet critical process that blends art and science. Unlike traditional valuation methods that rely heavily on financial metrics, startup valuation often focuses on potential rather than historical performance. For a SaaS company or any startup with no revenue, methods like comparable company analysis, discounted cash flows, and the development stage valuation approach are commonly used to estimate the company’s value. These valuation methods are crucial when pitching to venture capital firms, who often invest based on future growth potential rather than past performance.

By valuing a startup based on its expected future exit value and comparing it to similar companies, investors and founders can arrive at a more accurate valuation range. Whether you’re using the book value method, free cash flows, or a hybrid approach, the goal is to determine what your startup could be worth and ensure you receive the valuation you deserve. Ultimately, a well-executed valuation helps align expectations, secure funding, and execute the business plan, setting the stage for long-term success.

1. Checklist: Preparing for Startup Valuation

Goal: Gather data and minimize errors before calculations.

| Stage | Actions | Examples/Tips |

| Product Analysis | – Highlight technological advantages (patents, unique features). | Like DeepMind: Algorithms for playing Go. |

| – Prepare an MVP or prototype. | Even without revenue, like Uber in 2011. | |

| Team | – Showcase founders’ experience (ex-Google, Stanford, etc.). | A team of ex-Pfizer employees added $15 million to a biotech startup’s valuation. |

| Market | – Calculate TAM/SAM/SOM. | Uber: TAM $4.7T→$60M valuation. |

| – Study competitors. If there are none, emphasize this. | A platform for AI on quantum computers with no analogs. | |

| Metrics | – Collect data on CAC, LTV, retention rate. | A Silicon Valley startup improved its valuation by 40% after adjusting CAC. |

| Risks | – List risks (regulatory, technological). | A Miami crypto startup failed due to new SEC rules. |

2. Checklist: Choosing a Valuation Method

Goal: Select the right method and avoid subjectivity.

| Method | When to Use? | Check Questions |

| DCF | – If you have revenue forecasts for 3-5 years. | “What discount rate to apply? 25% or 30%?” |

| Market Multiples | – If there are comparable companies with known valuations (EV/Revenue, EV/EBITDA). | “What’s the current multiple? In 2022, EdTech dropped from 12x to 5x.” |

| VC Method | – If the investor has a clear target return (e.g., 5x in 5 years). | “What’s a realistic exit scenario? $100M sale or IPO?” |

| Hybrid Approach | – Combine methods for cross-verification. | DCF: $12M, Multiples:$15M. Final: $14M adjusted for patents. |

Tip: If the startup has no revenue, focus on TAM and team. Example: Uber’s $60M valuation based on the taxi market.

3. Checklist: Presenting Startup Valuation to Investors

Goal: Convince investors and avoid deal-breaking mistakes.

| Stage | Actions | Case Studies/Recommendations |

| Forecasts | – Ensure revenue growth is backed by metrics (virality >2, retention). | A California client failed after promising 500% growth without data. |

| Benchmarks | – Compare with 3-5 analogs. | “We’re like Shopify, but for online education.” |

| Story Over Numbers | – Tie valuation to a mission (“We’ll reduce CO₂ emissions by 1M tons”). | Airbnb: “We’re changing how people travel,” not “We rent out homes.” |

| Risks | – Add scenario analysis (“Even if the market drops 20%, we’ll survive”). | A Texas startup lost a deal due to an inflated TAM. |

| Q&A Prep | – Rehearse answers to: “How is TAM calculated?”, “Why is your CAC lower?”. | A Boston biotech startup explained patents in 2 minutes—secured $10M. |

Final Step: Check if your presentation includes:

- Real numbers (not “revenue will grow 300%,” but “15% monthly MRR growth”).

- Research references (“According to Crunchbase, SaaS startups grow 20% faster”).

- A call to action (“We need $2M to capture 5% of the market”).

How to Use the Checklists:

- Go through each stage sequentially.

- Refer to examples from the article (Uber, Airbnb, DeepMind).

- If something’s missing, revisit the comparison tables for methods and valuation factors.